News & Updates

The Passing of Jom Jacob, Co-founder and Chief Analyst of WhatNext Rubber Media International

It is with deep sadness that we announce the passing of Jom Jacob, our Chief Analyst and Co-founder of WhatNext Rubber Media International. Jom was a globally renowned rubber analyst with 36 years of unparalleled expertise, and his invaluable contributions have left an indelible mark on the industry.

Jom’s illustrious career included serving as Senior Economist at the ANRPC (Association of Natural Rubber Producing Countries) and as Deputy Director of Statistics and Planning at the Rubber Board. He was also a respected leader and former President of JCI Kottayam South. His vision, dedication, and passion shaped the growth of WhatNext and the global rubber community.

To all WhatNext members, please be informed that his monthly and weekly publications are temporarily discontinued until further notice. For any scheduled events, this announcement serves as an official notification of his unavailability. The WhatNext team will provide updates regarding future plans and membership details in due course.

We extend our heartfelt condolences to his family and request you to keep them in your thoughts and prayers during this difficult time.

Cup-lump Shortage Hits Liberia’s TSR Industry

Experts seek policy intervention to ban cup-lump exports

Block rubber or TSR processing factories in Liberia are increasingly challenged by a widening shortage of cup-lump in the country. With the recent opening of greenfield factories and capacity addition in the factories that existed from before, the country has the total capacity to produce 165,000 tons of TSR annually. To cater its TSR factories, the country annually needs around 254,000 tons of cup-lump (Measured in wet weight). However, the current level of domestic production of cup-lump is only around 185,000 tons (120,000 tons in dry weight) which represents only 65% of the quantity needed to run the factories. It means, operational efficiency and economic sustainability of the TSR factories in Liberia are increasingly challenged by an acute shortage of cup-lump. The following table helps to understand the gravity of the cup-lump shortage in the country.

| No. of shifts | Capacity of TSR Production (Tons/hour) | Annual Capacity, in tons (25 days/11 months) | Annual requirement of cup-lump (Wet weight in tons based on 65% dry rubber content) | |

| LAC | 3 | 5 | 33,000 | 50,770 |

| Firestone | 3 | 13 | 85,000 | 132,000 |

| Jeety Rubber | 3 | 5 | 33,000 | 50,770 |

| Lee | 2 | 3 | 13,200 | 20,300 |

| Nimba | 0 | 0 | – | – |

| All together | 26 | 165,000 | 253,840 |

Despite TSR factories facing such a huge shortage of raw material, a considerable portion of the domestic production of cup-lump goes out of the country by way of exports. To help the TSR processing factories have domestic availability of raw material, Liberia should immediately impose a total ban of exports. Such a policy intervention assumes significance from a wider developmental perspective on account of the following points:

- TSR processing factories in Liberia are compelled to scale down capacity utilization due to the domestic shortage of raw material. The lower capacity utilization impacts on the operational efficiency, unit cost of production, and global competitiveness of Liberian TSR. Persistent under-utilization of capacity poses a serious threat to the economic sustainability of TSR industry in the country.

- TSR processing factories in Liberia play a crucial role in the country’s rural employment generation, rural income and rural economic development. As an effective tool to strengthen rural economy and uplift the economic well-being of the rural community, government should consider strengthening the TSR processing factories by addressing the shortage of raw material.

- For the economic development of a country, value addition of raw materials should take place within the country. When value addition takes place within the country, it contributes to the economy by way of employment generation, development of ancillary sectors, and higher rural income. The higher rural income triggers rural demand for goods and services, and thereby contributes to the national economy. Higher rural income also contributes to the socio-economic uplift of economically weaker sections. Moreover, exports of value-added products bring much higher foreign exchange than raw materials.

It merits mention that Ivory Coast has imposed a ban on the exports of cup-lump from the country effective from 1 Jan 2024 as a measure to encourage domestic value addition. Due to the ban imposed by Ivory Coast, it is no longer possible for Liberia to bridge the shortage of cup-lump by importing from there. The recent capacity addition in TSR processing in Ghana and other West African countries signals that Liberia will not be able rely on these countries for sourcing cup-lump.

The above points justify the case for the Government of Liberia to ban the export of cup-lump and other unprocessed forms of natural rubber from the country with immediate effect.

#Liberia #BlockRubber #CupLump #RubberPolicy #WhatNextRubber #RuralDevelopment #RuralEconomy #MillenniumDevelopmentGoal #Commodity #ValueAddition #naturalRubber

India’s Sheet Rubber Market Misses the Global Rally. Is this a New Normal?

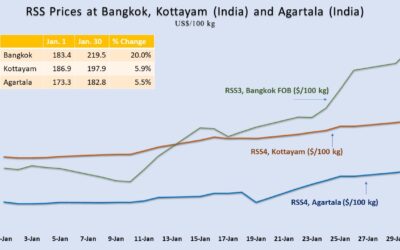

The prices of RSS3 at Bangkok FOB, the global benchmark grade of ribbed smoked sheet of natural rubber, soared 20% over the first 30 days of January 2024. RSS prices at Bangkok are poised to scale further up and continue along a rising curve for the next six months, as per the emerging supply-demand outlook from WhatNext Rubber Media.

Kottayam Market Stays almost Immune to Global Rally

In India, around 70% of the total production of natural rubber (NR) is processed and traded in the form of RSS. This is in sharp contrast with the global pattern where TSR or “block rubber” contributes around 65% of the output. “RSS4 at Kottayam” is India’s benchmark reference price for NR (Kottayam is the largest NR producing district in the State of Kerala, the traditional rubber-growing region of India). Surprisingly, RSS4 prices at Kottayam rose only 6% during the first 30 days in Jan 2024 against a 20% jump at Bangkok market during the same period. Kottayam market used to rule above the Bangkok market by 20% to 30%. Moreover, Kottayam market used to track the rally at Bangkok market. In sharp contrast with the earlier pattern, Kottayam market stayed almost immune to the sharp gains at Bangkok market in January. Moreover, Bangkok market crossed over Kottayam market on January 12, 2024. (Please see the chart given above). What are the factors that prevented Kottayam market from gaining in tandem with the 20% surge at Bangkok market? Is this a temporary phenomenon, or a new normal?

Indian Auto-Tyre Industry Shifts from RSS to TSR

A comparison between the RSS markets in India and Thailand used to be relevant during the past when Indian auto tyre manufacturing companies predominantly consumed RSS unlike the TSR-dominant manufacturing followed by their counterparts outside the country. Over the past nearly 10 years, the Indian auto tyre companies have largely shifted to a TSR-based manufacturing by deviating from the hitherto followed RSS-based manufacturing. Because of the RSS-based manufacturing followed in the past, auto-tyre companies in the country used to source NR after making a comparison between the cost of domestic RSS and imported RSS. That practice has changed over the past 10 years due to the shift from RSS to TSR. The Indian auto tyre manufacturing industry currently turns to domestic RSS only is it is economically more attractive than souring TSR from overseas. It means, the cost of imported RSS is no more relevant to the Indian auto-tyre companies due to the shift to TSR. The prices of TSR are considerably below RSS prices. The point is that the shift from RSS to TSR by the Indian auto-tyre manufacturing companies has made Kottayam RSS market almost insensitive to the RSS market at Bangkok.

Sourcing Shifts from Indonesia to Ivory Coast

Auto-tyre manufacturing companies in India have recently shifted their sourcing of TSR. Earlier they used to source TSR largely from Indonesia and other southeast Asian NR producing countries. Ivory Coast has become the preferred source for the Indian auto tyre companies for sourcing TSR over the past two years. It means that auto-tyre manufacturing companies in India currently source RSS from domestic market only if they find it more economic than souring TSR from Ivory Coast. From this perspective, it is the TSR prices prevailing in Ivory Coast that influences the Kottayam RSS market rather than the RSS prices at Bangkok. The close link between the Indian RSS market and the Bangkok RSS market is a story of the past which is no more relevant in the changed scenario.

Increasing Influence of Low-Cost Rubber from Northeast India

In meeting the demand for RSS, Indian tyre industry can now increasingly rely on northeast India which is a non-traditional region having considerable cost advantage over the traditional region (State of Kerala). In the northeast India, the prices of RSS4 (Agartala Market is the reference market for northeast India) are around 10% lower compared to Kottayam. India’s northeast currently accounts for around 20% of the country’s total output of NR. As a new trend, major auto tyre manufacturing companies currently bring RSS from northeast India to their factories located in Kerala because of the substantial cost advantage. It means, the RSS market in Kerala currently faces competition not from imported RSS, but from the RSS produced within India, in the country’s northeast, at a substantially lower cost. The low-cost RSS coming from northeast India is exerting a downward pressure on RSS market in the traditional region, especially the State of Kerala. This trend in expected to continue with an increasing influence. It means, it’s not a temporary happening, but a new normal.

Northeast India to Contribute more than 50% of India’s Rubber Output

The Rubber Board, by joining hands with India’s Auto Tyre Manufacturers’ Association (ATMA), has launched a massive rubber cultivation project in northeast India envisaging expansion of rubber cultivation by 200,000 hectares by 2025. This can bring an additional output of around 300,000 tons per year when the planted trees attain maturity by early 2030s. With this additional production, the share of northeast India in the country’s total production is expected to go beyond 50%, from the current level of 20% (Northeast India is projected to produce around 525,000 tons of NR by 2032 if the ongoing planting programme in the region achieves the target). It means, the Kottayam RSS market should expect more dominating negative influence of the low-cost RSS coming from northeast India in the years ahead.

Kerala’s Shrinking Rubber Map

With the increasing dominance of low-cost NR from northeast India, rubber farmers in the State of Kerala will be ultimately left with no option but selling the produce at prices matching with those prevailing at Agartala. The dominating influence of low-cost NR from northeast India, along with the abnormally high wages in Kerala, higher cost of material inputs, and a considerably lower purchasing power of rupee in the state, will make rubber cultivation economically unviable in Kerala. It means, parallel to the expansion of cultivation in the northeast India, Kerala should expect a marked shrinkage of rubber area. The possibility of Kerala getting almost fully wiped out from India’s natural rubber production map cannot be ruled out.

Prices are Right for Exports

Conditions are now ideal for India to exploit the higher RSS prices overseas. The wide gap between the RSS prices at Kottayam and Bangkok, and that between Agartala and Bangkok, offer immense scope for India to tap the global rally in RSS prices and thereby support the farmers. A policy initiative along this direction can also help Indian RSS market to gain momentum and move in tandem with the surging Bangkok market.

Get in Touch. Get Involved.

Vivamus suscipit tortor eget felis porttitor volutpat. Nulla quis lorem ut libero malesuada feugiat. Vivamus suscipit tortor eget felis porttitor volutpat. Proin eget tortor risus.